Tap-to-pay vs card insertion: which one actually protects you from fraud

You stand at the checkout, card in hand, staring at the terminal. Tap or insert? The cashier doesn't care. The line behind you is growing. You pick one and hope it's the right choice.

The question isn't just about speed. It's about security. Tap-to-pay and chip insertion both claim to protect you from fraud, but they work differently. One generates a one-time token that expires after the transaction. The other does the same thing through a different mechanism. Both are light-years ahead of magnetic stripe swipes, which transmit your actual card number every time.

Here's how each method handles your payment data, what attackers can steal, and which vulnerabilities matter in 2026.

How tap-to-pay actually works

Tap-to-pay uses Near Field Communication (NFC), the same technology that powers keyless entry cards and transit passes. When you hold your card or phone near the terminal, the two devices exchange encrypted data over a radio frequency connection. The range is short, around four inches maximum. Beyond that distance, the signal weakens to nothing.

Your card doesn't transmit your actual card number during a tap transaction. Instead, it generates a one-time token called a cryptogram. This token contains transaction-specific information: the amount, the merchant identifier, a timestamp, and a unique code that can only be used once. The token goes to your bank, which verifies it and approves the payment. After that, the token becomes worthless. An attacker who intercepts it can't replay it, can't use it at another merchant, can't extract your card number from it.

The cryptogram generation happens inside a secure element, a dedicated chip in your card or phone that stores your payment credentials in encrypted form. This chip is physically separate from your phone's main processor. Even if malware compromises your phone's operating system, it can't reach the secure element. Apple Pay, Google Pay, and Samsung Pay all use this architecture.

When you tap your phone to pay, the system requires authentication before it generates the token. Face ID, Touch ID, or a PIN. Without unlocking the device, the secure element won't release the payment credentials. A thief who steals your phone can't tap it to buy things unless they can also unlock it.

Tap-to-pay transactions are capped at specific amounts in many regions, around $100 to $250, depending on the country and the card network. Transactions above that threshold require a PIN or signature. This limit exists to reduce the impact of a stolen card being used before the cardholder notices and reports it.

How chip insertion works

EMV chip cards, named after Europay, Mastercard, and Visa, the organizations that developed the standard, also generate one-time tokens. The mechanism is similar to tap-to-pay, but the communication happens through physical contact between the chip and the terminal's reader.

When you insert your card, the terminal sends a challenge to the chip. The chip processes this challenge using a cryptographic algorithm and your card's unique key, then generates a response. This response is the token. It's specific to this transaction, this terminal, this amount, this moment. The terminal forwards the token to your bank, which verifies it and approves or declines the payment.

The chip never transmits your card number in cleartext. It never transmits the CVV code printed on the back of your card. It never transmits static data that an attacker could reuse. The token it generates is worthless after the transaction completes.

Chip cards require you to leave the card inserted until the transaction finishes. This takes longer than tapping, typically three to five seconds instead of one. The delay comes from the cryptographic computation happening inside the chip and the back-and-forth communication with the terminal. The chip is a tiny computer running security protocols, and those protocols take time.

Some chip cards also support contactless payment. These are called dual-interface cards. They have both a chip for insertion and an NFC antenna for tapping. The two interfaces use the same secure element and generate tokens the same way. The only difference is how the card communicates with the terminal.

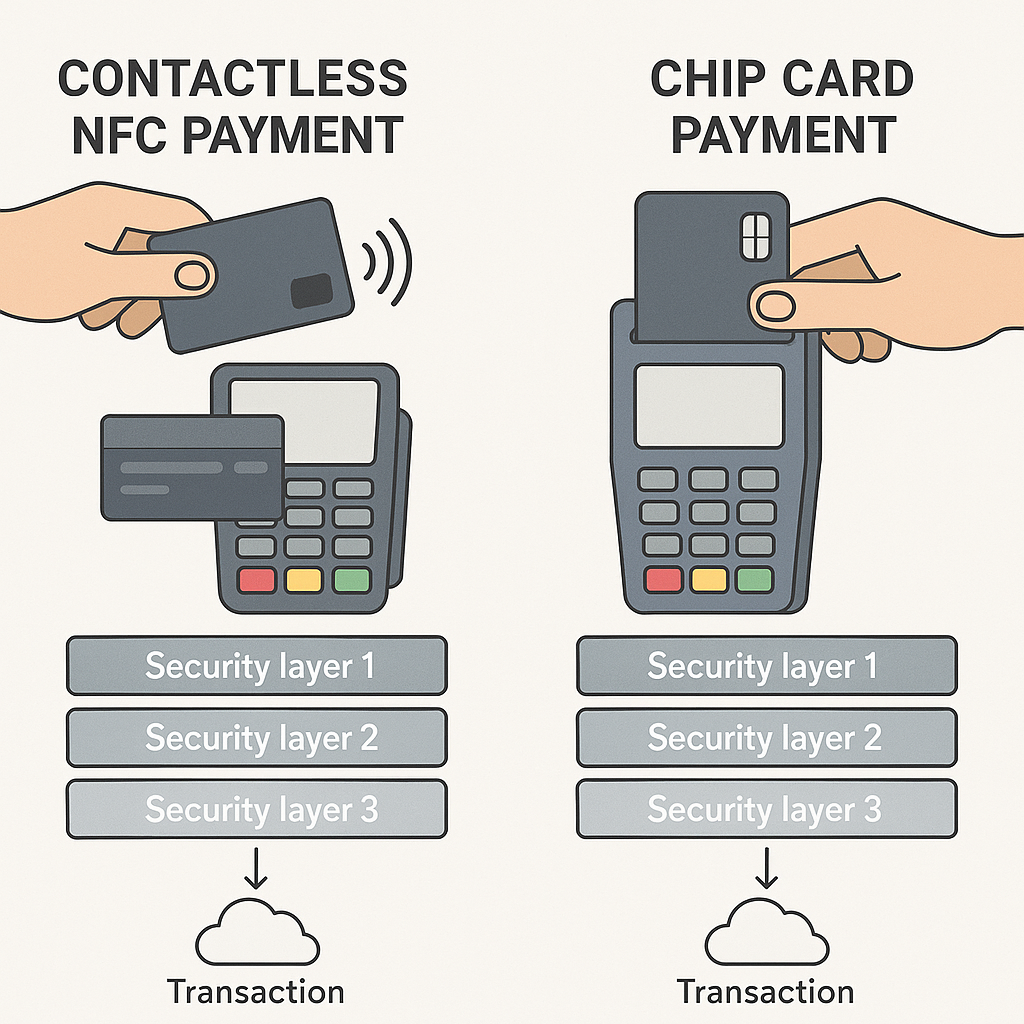

What attackers can steal from each method

Skimmers, devices that criminals attach to payment terminals to steal card data, can't capture tap-to-pay or chip transactions. Skimmers work by reading the magnetic stripe on the back of your card, which contains your card number, expiration date, and cardholder name in cleartext. When you tap or insert, the magnetic stripe isn't involved. The token that gets transmitted is useless to a skimmer because it can't be reused.

Relay attacks are a theoretical threat against tap-to-pay. An attacker places one device near your card to capture the NFC signal, then relays it to a second device at a merchant terminal. This would allow them to make a purchase using your card without physically stealing it. In practice, relay attacks are difficult to execute. The attacker needs two devices, precise timing, and proximity to both your card and a payment terminal at the same moment. Researchers have demonstrated relay attacks in controlled environments, but documented cases of real-world relay fraud are rare.

Chip insertion is immune to relay attacks because the card must be physically present in the terminal. The communication happens through direct contact, not radio waves. An attacker can't relay a signal that requires metal-to-metal connection.

Malware that targets point-of-sale systems can potentially capture payment data, but only if the terminal is compromised before the encryption happens. Modern terminals encrypt the transaction data immediately after the chip or NFC reader captures it. If malware runs on the terminal, it might see encrypted data, but it can't decrypt it without the terminal's cryptographic keys. Those keys are stored in a secure module inside the terminal, separate from the main processor.

The bigger vulnerability for both tap and chip is the merchant's backend systems. After your bank approves the transaction, the merchant stores a record of it. That record might include your card's last four digits, the transaction amount, the date, and your name. If the merchant's database gets breached, attackers can access this information. They can't use it to make fraudulent charges directly, but they can use it for social engineering attacks or identity theft.

Fraud liability and what you actually pay for

Federal law limits your liability for unauthorized credit card charges to $50. Most card issuers go further and offer zero-liability policies, meaning you pay nothing if someone uses your card fraudulently. This applies to both tap-to-pay and chip insertion. The method doesn't change your legal protection.

Debit cards have different rules. If you report unauthorized charges within two business days, your liability is capped at $50. If you wait longer than two days but report within 60 days, your liability can go up to $500. After 60 days, you might be liable for all unauthorized charges. The Electronic Fund Transfer Act sets these limits, and they apply regardless of whether the fraud happened through tap, chip, or swipe.

When you dispute a charge, your bank investigates. They look at the transaction data to determine whether the charge was authorized. Tap-to-pay and chip transactions include more data points than magnetic stripe swipes, timestamps, merchant identifiers, cryptographic tokens, which makes it easier for banks to detect fraud patterns. If your card was physically present at a terminal and the chip or NFC reader authenticated the transaction, the bank's fraud detection system is more likely to flag it as legitimate unless other indicators suggest otherwise.

Chargebacks, disputes you file with your bank to reverse a charge, work the same way for tap and chip. You contact your bank, explain why the charge is unauthorized, and the bank investigates. If they rule in your favor, they reverse the charge and issue a credit to your account. The merchant can contest the chargeback, but the burden of proof is on them to show that the transaction was legitimate.

What merchants see and what they don't

When you tap or insert your card, the merchant's terminal captures the transaction data and sends it to the payment processor. The merchant never sees your full card number. They see the last four digits, the card network (Visa, Mastercard, etc.), and the transaction amount. The one-time token that authorizes the payment goes directly to your bank through the payment network. The merchant doesn't have access to it.

This is why data breaches at retailers don't usually compromise tap-to-pay or chip transactions. The merchant's database contains transaction records, but those records don't include the cryptographic tokens or your full card number. Attackers who breach the database get the last four digits of your card and the transaction history, but they can't use that information to make fraudulent charges.

Magnetic stripe data is different. When you swipe your card, the terminal reads the full card number, expiration date, and cardholder name from the stripe. Some merchants store this data, which is why breaches of retailers that still use swipe-only terminals can result in large-scale card fraud. The attackers get full card numbers that they can use to make online purchases or create counterfeit cards.

The actual risks you face in 2026

Tap-to-pay and chip insertion both protect you from the most common types of card fraud: skimming, counterfeit cards, and replay attacks. The vulnerabilities that remain are mostly outside the payment transaction itself.

Phishing attacks that trick you into giving up your card number still work. If you type your card number into a fake website or tell it to a scammer over the phone, neither tap nor chip can protect you. The fraud happens before the payment method is involved.

Account takeover attacks, where an attacker gains access to your online banking or card issuer account, bypass the security of physical payments entirely. If someone logs into your account and requests a new card or changes your contact information, the security of tap-to-pay or chip insertion doesn't matter.

Lost or stolen cards are still a risk, but the exposure is limited. If someone steals your contactless card, they can make small purchases under the tap-to-pay limit before you report it. If they steal your chip card, they need your PIN to make purchases, unless the merchant allows chip-and-signature transactions. Most U.S. merchants still accept signatures instead of PINs, which reduces the security benefit of chip cards.

Phone-based tap-to-pay is more secure than a physical card in the case of theft, because the phone requires biometric authentication or a PIN for each transaction. A stolen phone without the unlock code can't be used to make payments.

Which method to use and when

If the terminal supports both tap and chip, tap is faster and equally secure. The transaction completes in around one second instead of three to five. The security mechanisms are equivalent, both generate one-time tokens, both protect your card number, both offer the same fraud liability.

If you're making a purchase above the contactless limit, the terminal will prompt you to insert your card or enter a PIN. This is a policy decision by the card networks to reduce fraud risk on high-value transactions. The limit varies by region and by card issuer, but it's typically in the $100 to $250 range.

If you're using your phone to pay, tap is your only option. Apple Pay, Google Pay, and Samsung Pay all use NFC. They don't support chip insertion because phones don't have chip readers.

If the terminal doesn't support contactless payments, you'll have to insert your card. Some merchants haven't upgraded their systems, and some terminals disable contactless functionality even though the hardware supports it. This is usually a cost decision, contactless terminals can be more expensive, and some merchants prioritize other investments.

Magnetic stripe swipes should be your last resort. If a terminal only supports swipe, your card number is transmitted in cleartext and stored by the merchant. This is the highest-risk payment method still in use. If you have the option to insert or tap, use it.

What happens when something goes wrong

If you notice a fraudulent charge on your card, report it immediately. Contact your card issuer's fraud department, the phone number is on the back of your card. They'll freeze your card, investigate the charge, and issue a new card with a different number.

The FTC's fraud reporting platform allows you to file a report about the incident. This doesn't directly reverse the charge, but it helps law enforcement track fraud patterns and can support your case if the issuer disputes your claim.

If the fraudulent charge was made in person using tap-to-pay or chip insertion, the investigation will focus on how the attacker obtained your card or your phone. If your card was stolen and used before you reported it, you're covered by the zero-liability policy. If your phone was stolen and used, the investigation will examine whether the attacker bypassed your phone's security, biometric authentication or PIN.

If the fraudulent charge was made online, the payment method doesn't matter. Online transactions don't use tap or chip. They use the card number, expiration date, and CVV code. If an attacker has that information, they can make purchases without your physical card.

Disputing a charge doesn't affect your credit score. The dispute process is separate from credit reporting. Your card issuer might place a temporary hold on your account while they investigate, but this doesn't appear on your credit report.

The infrastructure gap that still exists

Not all merchants accept contactless payments, even in 2026. Some terminals don't have NFC readers. Some merchants disable contactless functionality because they don't want to pay the processing fees, which can be slightly higher than chip transactions. Some point-of-sale systems are old and haven't been upgraded.

This creates a security gap. When you're forced to swipe your card because the terminal doesn't support chip or tap, your card number is exposed. Skimmers can capture it. The merchant's database stores it. If the merchant gets breached, your card number is part of the compromised data.

The U.S. is behind other countries on contactless adoption. In the UK, Australia, and Canada, contactless payments are the default. Most terminals support tap, and most consumers use it. The U.S. still has a significant number of swipe-only terminals, particularly at small businesses and older gas stations.

Gas station pumps are a specific problem. Many pumps still use magnetic stripe readers, even though the pump hardware could support chip or contactless. The delay in upgrading gas station payment systems is partly due to cost, replacing a pump's payment hardware is expensive, and partly due to regulatory deadlines that keep getting extended. As of 2026, many gas stations still accept swipe-only payments.

The question you actually asked

Is tap-to-pay safer than card insertion? They're equivalent. Both generate one-time tokens. Both protect your card number. Both offer the same fraud liability. The difference is speed and convenience, not security.

The real security gap is between chip/tap and magnetic stripe. If you're still swiping your card, you're exposing your card number every time. Upgrade to a chip card if you haven't already. Use tap-to-pay when the terminal supports it. Avoid swipe whenever possible.

If your card gets stolen, report it immediately. If you see a fraudulent charge, dispute it. If you're forced to swipe at a sketchy-looking terminal, check your account the next day. The security mechanisms built into tap and chip can't protect you from every threat, but they eliminate the most common ones.

The choice between tap and insert doesn't matter as much as the choice between chip/tap and swipe. That's the decision that actually affects your fraud risk.