Credit Monitoring Services Compared: Which One Actually Protects You

You check your credit score every few months. Maybe you signed up for one of those free monitoring services after a breach. Maybe your bank offers it as a perk. Maybe you're paying $20 a month for something that promises to watch your credit around the clock.

Credit monitoring services all claim to protect you from identity theft, but what they actually monitor, how quickly they alert you, and what happens after an alert varies dramatically. Some services watch one bureau. Others watch all three. Some send alerts within hours. Others take days. Some include identity theft insurance. Others just send you an email and leave you to figure out what comes next.

I've spent two decades writing about identity theft for security vendors, and the one thing I've learned is that credit monitoring is misunderstood more often than it's explained clearly. People think it prevents fraud. It doesn't. It detects fraud after someone has already used your information. That distinction matters, because what you do with the alert determines whether you catch the problem early or spend months cleaning up the damage.

This article compares the major credit monitoring options: free services from Equifax, Experian, and TransUnion, free third-party services like Credit Karma, and paid services like NordProtect. Here's what each one monitors, how the alerts work, and which makes sense for your situation.

What Credit Monitoring Actually Does

Credit monitoring is a notification system. It watches your credit file at one or more bureaus and sends you an alert when something changes. The change could be a new account, a credit inquiry, a balance increase, a late payment, or an address update. The service doesn't stop the change from happening. It tells you the change happened so you can verify it's legitimate.

The underlying mechanism is straightforward. The monitoring service checks your credit report regularly, daily for most paid services, less frequently for free ones, and compares the current version to the previous version. When it detects a difference, it sends you an email, text, or app notification describing what changed.

The value of credit monitoring depends on two things: how quickly you get the alert, and what you do with it. If you get an alert about a new credit card you didn't open, you can contact the issuer immediately, freeze your credit, and file a fraud report before the thief racks up charges. If you ignore the alert or don't see it for weeks, the damage spreads.

Credit monitoring doesn't prevent identity theft. It doesn't block fraudulent applications. It doesn't stop someone from using your Social Security number to open accounts. What it does is compress the window between when fraud occurs and when you find out about it. That window matters, because the longer fraud goes undetected, the harder it is to unwind.

Free Credit Monitoring from the Bureaus

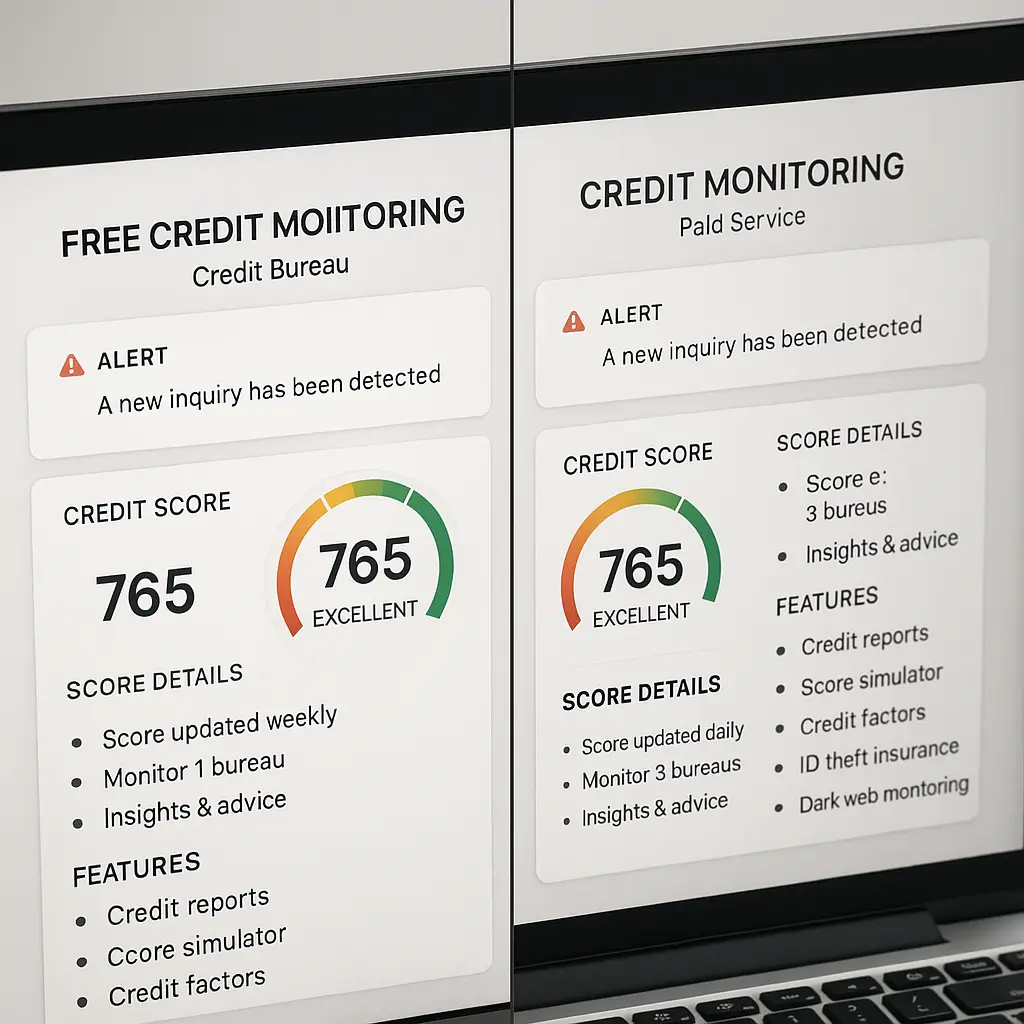

Equifax, Experian, and TransUnion all offer free credit monitoring services. Each service monitors only that bureau's credit file. If you sign up for Experian's free monitoring, you'll get alerts when something changes on your Experian report, but you won't hear about changes to your Equifax or TransUnion reports unless you sign up for those separately.

The alerts cover new accounts, credit inquiries, balance changes, and late payments. Most services send alerts within 24 hours of the change appearing in your credit file, though timing varies depending on when the lender reports the activity to the bureau. You'll also get access to your credit score from that bureau, updated monthly or quarterly depending on the service.

What you don't get with free bureau monitoring is coverage across all three bureaus. Not all lenders report to all three bureaus, so fraud that appears on your Equifax report might not show up on Experian or TransUnion. If you're only monitoring one bureau, you'll miss fraud reported to the other two. That's not a hypothetical risk, around 30 percent of consumers have material differences between their credit reports at the three bureaus, according to research cited by the FTC.

Free bureau monitoring also doesn't include identity theft insurance, dark web monitoring, or recovery support. If you get an alert about fraud, you're on your own to figure out what to do next. The bureau will point you to IdentityTheft.gov for guidance, but you'll be handling the dispute process, the fraud affidavits, and the follow-up yourself.

Free bureau monitoring makes sense if you're willing to sign up for all three bureaus separately and you're comfortable handling fraud recovery on your own. It's free, it covers the basics, and it gives you visibility into what's happening with your credit. But it requires you to manage three separate accounts, remember three separate logins, and piece together a complete picture from three different sources.

Credit Karma and Other Free Third-Party Services

Credit Karma offers free credit monitoring that covers two bureaus: TransUnion and Equifax. You get alerts when something changes on either report, access to your credit scores from both bureaus, and a dashboard that consolidates everything in one place. The service is free because Credit Karma makes money by recommending credit cards, loans, and financial products based on your credit profile.

The monitoring works the same way as the bureau services, Credit Karma checks your reports regularly and sends alerts when changes appear. The advantage over free bureau monitoring is that you're watching two bureaus instead of one, which catches more fraud. The disadvantage is that you're still missing Experian, and you're trusting a third party with access to your credit data.

Other free third-party services work similarly. Some monitor two bureaus, some monitor one, and all make money by showing you offers for financial products. The alerts are legitimate, the monitoring is real, but you're trading your attention, and your willingness to see targeted offers, for the service.

Free third-party monitoring makes sense if you want coverage across multiple bureaus without paying for it and you're comfortable with the trade-off. You'll see ads. You'll get recommendations for credit cards you might not need. But you'll also get alerts when something changes on two of your three credit reports, which is better than monitoring just one.

Paid Credit Monitoring Services

Paid credit monitoring services typically monitor all three bureaus, send faster alerts, and include additional features like dark web monitoring, identity theft insurance, and recovery support. Services like NordProtect charge around $10 to $20 per month and promise to watch your credit, scan data broker sites for your personal information, and alert you if your email or Social Security number appears in a breach.

The core value of paid monitoring is three-bureau coverage. Instead of signing up for three separate free services or accepting two-bureau coverage from Credit Karma, you get one dashboard that shows you everything. When a new account appears on any of your three credit reports, you get an alert. When a hard inquiry shows up, you get an alert. When your address changes, you get an alert.

Paid services also tend to send alerts faster than free services. Some promise near-real-time notifications, though "real-time" still depends on when the lender reports the activity to the bureau. If a fraudulent account doesn't show up on your credit report for three days, no monitoring service, free or paid, will alert you before those three days pass.

Beyond credit monitoring, paid services often include dark web scanning, which searches breach databases and underground forums for your email address, Social Security number, and other personal information. If your data appears in a new breach, you get an alert. Some services also offer identity theft insurance, which covers expenses like legal fees, lost wages, and document replacement if you become a victim of identity theft. The insurance doesn't reimburse stolen money, your bank or credit card issuer handles that, but it covers the costs of cleaning up the mess.

Recovery support is another feature that separates paid services from free ones. If you get an alert about fraud, paid services often provide access to fraud resolution specialists who walk you through the dispute process, help you file reports, and follow up with creditors on your behalf. That support doesn't prevent fraud, but it reduces the time and stress involved in recovering from it.

Paid credit monitoring makes sense if you want comprehensive coverage without managing multiple accounts and you value the extra features like dark web scanning and recovery support. It's not a replacement for a credit freeze, monitoring alerts you after fraud occurs, while a freeze prevents new accounts from being opened in the first place, but it's a useful layer of defense if you're not ready to freeze your credit or if you need to keep your credit accessible for legitimate applications.

What Credit Monitoring Doesn't Catch

Credit monitoring only detects fraud that shows up on your credit report. If someone steals your tax refund by filing a fraudulent return, credit monitoring won't alert you. If someone uses your health insurance to get medical care, credit monitoring won't catch it. If someone opens a utility account in your name, credit monitoring might not see it unless the utility reports to the credit bureaus, and many don't.

Credit monitoring also doesn't catch fraud instantly. There's always a delay between when fraud occurs and when it appears on your credit report. A thief opens a credit card in your name today. The issuer processes the application, approves it, and reports the new account to the bureaus. That reporting might happen within 24 hours, or it might take a week. Your monitoring service checks your report and sends you an alert. By the time you see the alert, the account has already been open for days, and the thief might have already maxed it out.

That delay is inherent to the system. Credit monitoring is reactive, not proactive. It tells you something happened. It doesn't stop it from happening. That's why credit monitoring works best in combination with other protections like credit freezes, strong passwords, and careful handling of your Social Security number.

Comparing the Options: What You Actually Get

Here's how the major credit monitoring options compare on the features that matter:

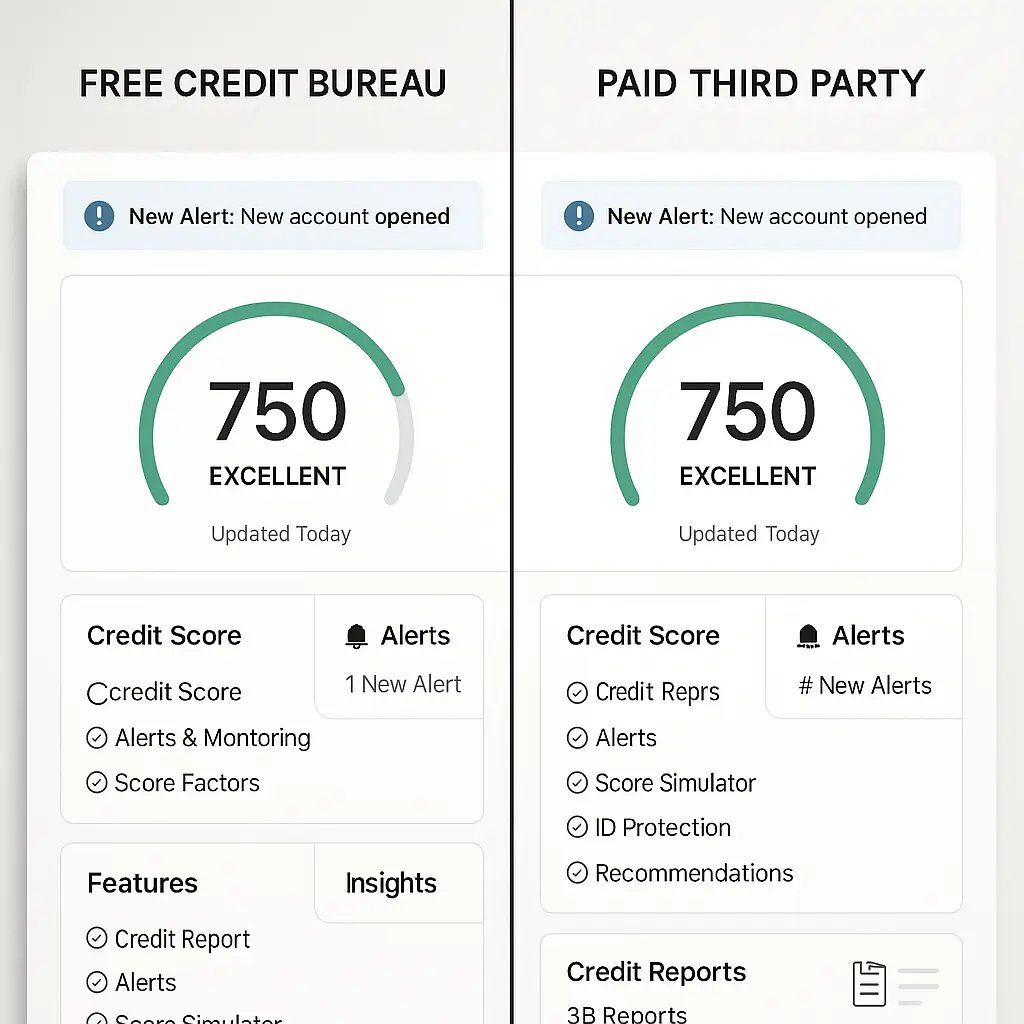

Free bureau monitoring (Equifax, Experian, TransUnion): Monitors one bureau per service. Alerts within 24 hours of changes. Access to your credit score from that bureau. No dark web scanning, no identity theft insurance, no recovery support. You handle fraud on your own.

Free third-party monitoring (Credit Karma, others): Monitors two bureaus (typically TransUnion and Equifax). Alerts within 24 hours. Access to credit scores from both bureaus. Dashboard consolidates both reports. No dark web scanning, no identity theft insurance, no recovery support. You'll see targeted offers for financial products.

Paid monitoring (NordProtect, others): Monitors all three bureaus. Alerts within 24 hours, sometimes faster. Access to credit scores from all three bureaus. Dark web scanning for your email, Social Security number, and other personal data. Identity theft insurance covering recovery expenses. Access to fraud resolution specialists who help with disputes and recovery.

The choice depends on what you're trying to protect against and how much you're willing to pay. If you're monitoring credit because you're worried about a specific breach or because you've been a victim of identity theft before, three-bureau coverage makes sense. If you're monitoring credit as a general precaution and you're comfortable managing fraud recovery yourself, free monitoring from the bureaus or Credit Karma gets you most of the way there.

How to Choose a Credit Monitoring Service

Start by asking what you're actually trying to accomplish. If your goal is to catch fraud early so you can shut it down before it spreads, you need three-bureau coverage. Monitoring just one bureau leaves gaps. Monitoring two bureaus is better, but you're still missing one-third of the picture.

If your goal is to track your credit score and get notified when something changes, free bureau monitoring or Credit Karma works fine. You'll get alerts, you'll see your score, and you'll have enough information to spot obvious fraud. You won't have the same level of coverage as a paid service, but you'll have enough to catch most problems.

If you've been a victim of identity theft before, if you've been involved in a major breach, or if you're in a high-risk category, like someone whose Social Security number has been exposed in multiple breaches, paid monitoring with recovery support makes sense. The extra features won't prevent fraud, but they'll make it easier to deal with when it happens.

Don't assume credit monitoring replaces other protections. A credit freeze is still the strongest defense against new account fraud. Two-factor authentication still protects your online accounts. A password manager still prevents credential stuffing. Credit monitoring is one layer in a larger system. It's useful, but it's not a replacement for the other steps.

What to Do When You Get a Fraud Alert

When you get an alert about suspicious activity, act immediately. Don't wait to see if it's legitimate. Don't assume it's a mistake. Check your credit report, verify whether you recognize the activity, and if you don't, start the dispute process right away.

IdentityTheft.gov walks you through the exact steps: file a report with the FTC, place a fraud alert with one of the credit bureaus (which automatically notifies the other two), contact the company where the fraud occurred, and dispute the fraudulent information on your credit report. If you're using a paid monitoring service with recovery support, call them first and let them guide you through the process.

The faster you act, the less damage the fraud causes. If you catch a fraudulent credit card within days of it being opened, you can close it before charges accumulate. If you catch it weeks later, you're dealing with maxed-out limits, late payments, and a bigger mess to clean up.

The Reality Behind Credit Monitoring

Credit monitoring doesn't prevent identity theft. It detects it. That distinction matters because people buy monitoring services thinking they're buying protection, and they're not. They're buying a notification system that tells them when something has already gone wrong.

That notification system is valuable, catching fraud early reduces damage, but it's not a substitute for prevention. A credit freeze prevents new accounts from being opened in your name. Credit monitoring tells you after they've been opened. Both tools serve a purpose. Neither replaces the other.

If you're trying to decide whether to pay for credit monitoring, ask yourself how quickly you'd notice fraud without it. If you check your credit reports regularly, if you review your bank statements every week, if you're vigilant about watching for signs of identity theft, free monitoring might be enough. If you're not that vigilant, if you're worried about missing something, if you want someone else to watch your credit for you, paid monitoring makes sense.

Credit monitoring is a tool. It's not a solution. It's not a guarantee. It's a way to compress the time between when fraud happens and when you find out about it. That compression matters, but it only matters if you act on the alerts when they arrive.